As we near the halfway mark this year, the Association for Cultural Enterprises Commercial Performance Barometer suggests performance has been mixed. Admissions are struggling but other commercial areas are compensating for fewer people through the doors.

Key findings include:

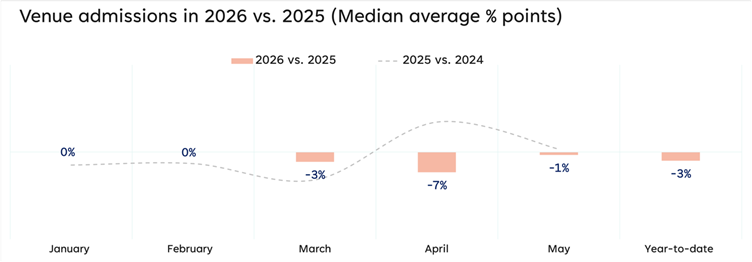

- Year-to-date admissions are -3% down on 2025, driven by general visitors and a slight drop in organised groups

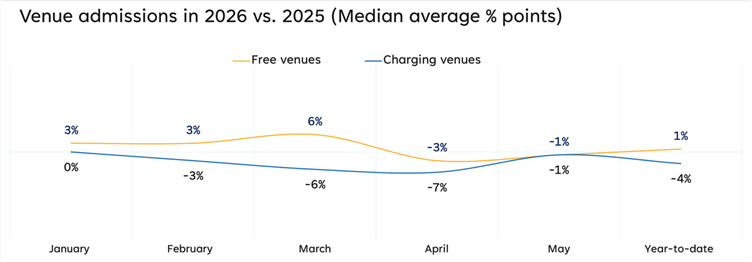

- Struggling admissions are driven by charging venues (-4%); free venues are slightly up on last year (+1%)

- Weather, cost-of-living and global instability remain the key drags on visitation

- Catering, retail, events and venue hire are each performing ahead of 2025

- Innovative marketing is playing a key supporting role

Admissions

In our last blog in April we reported on a slow first quarter, not helped by Easter storms and snow (hard to believe as some of us are still recovering from a second heatwave!). A few months on, the story is relatively similar, with cultural venues consistently reporting lower admissions than in 2025.

At a UK level, visits are -3% down and (with the exception of Northern Ireland), there is no evidence of any regions bucking the trend. These figures come against the backdrop of a 2025 that endured a similarly poor January to March, but experienced a mini revival in April and May.

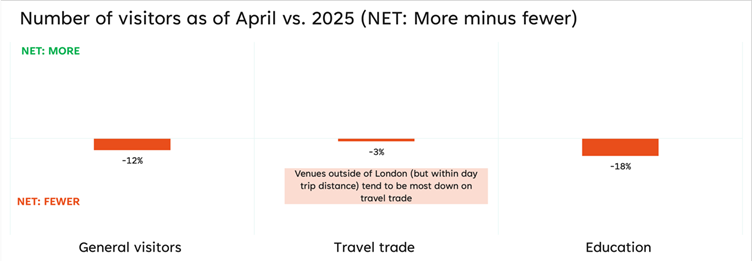

The fall in visitors is most evident amongst ‘general visitors’, but venues also report a slight drop in organised groups (particularly places within daytrip distance of London), and a large drop amongst education visits.

Don’t mention the weather

In recent weeks there have been more than a few comment pieces from ex-Merlin employees describing how weather was ‘banned’ as an excuse for poor performance in their day. But it’s very hard to look past meteorological factors in an era where each month seems to welcome devastating storms or record temperatures.

Participants in the Barometer seem to agree. Weather was by far the most stated driver of performance in May, with 39% mentioning it negatively, and just 7% positively. One indoor venue stated:

“The heatwave over the half term holiday decimated visitor numbers on what is traditionally a key trading period. Whilst usually quieter than the February and October half terms, visitor numbers did not increase at all over the May half term and matched term time figures for the rest of the month, making it the lowest May half term in a decade (excluding Covid).”

While good weather is often a windfall for outdoor venues, there is a tipping point where everyone suffers, and it feels as if this threshold was crossed in May half term – as indicated by one outdoor attraction:

“We were tracking well above YTD trend until the heatwave in the early part of the half term. Attendance dropped to term time levels and hit additional spend as well. We didn’t recover, and ended 2,500 visitors down on May half term 2025.”

Cost-of-living impact is clear

Without instant market research it’s hard for cultural venues to understand the impact of personal finances on visit patterns, but as of the end of May, our data tells a clear story. Charging venues are consistently reporting worse admissions than free venues, with the former -4% down, and the latter actually 1% up on 2025. The picture appears to get more negative the higher the price point – in England, charging venues that attract over 500k visitors (a proxy for more expensive entry) are -8% down YTD.

In 2025, a similar (albeit less stark) gap was overcome by successful programming, particularly in the summer and winter months. Fingers crossed we see a similar outcome in 2026.

Revived retail countering poor footfall

While weak admissions are a cause for concern, it’s reassuring to see positive commercial figures elsewhere. Similar to last year, catering is performing well, with SPV +6% vs 2025, and ATV +4%. Most positively, we are seeing strong growth in retail, with SPV +6%, and ATV +2% on 2025.

The positive performance of retail marks a reversal on what we saw throughout last year and perhaps points to a concerted effort from the sector to address this issue.

Venue comments support this hypothesis, with retail mentioned positively amongst 17% of participants in May. In most of these cases strong retail spend is driven by commercially-friendly exhibitions, suggesting that commercial teams are increasingly being given a seat at the table when programming decisions are made (see our report for more on this).

“Retail performance has been exceptional in May thanks to a highly commercial exhibition, Handpicked: Painting Flowers 1900-Today. It’s not just the increased footfall – it’s bringing in an audience demographic that really spends in the shop.” (Kettle’s Yard)

“New high season summer fashion exhibition launched in May. A retail range was introduced to complement the exhibition and a bespoke cabinet created that sits outside of the retail store and so really draws the eye of visitors in the Atrium. The ranges have proven to be very popular.” (Titanic Belfast)

“Strong retail performance driven by programming with a strong commercial aspect.” (St Albans Museum + Gallery)

“Our temporary exhibition on Leonora Carrington has been a great success. We have been selling the exhibition catalogues, the exhibition related books and art prints.” (The Freud Museum)

“Retail-wise, and I don’t want to jinx it, but there may be small signs of recovery. The figures are less bad than the previous months. This is likely to do with a new exhibition opening.” (The Cartoon Museum)

“In Bloom is a popular exhibition with strong ticket sales and footfall and this is driving positive results for both catering and retail shop spend.” (The Ashmolean)

Events and venue hire also contributing positively

In May’s Barometer, ‘net’ 33% said their events programme was performing better than in 2025. A combination of family programming, festivals and partnerships all played a role.

“Visitor numbers were higher as we hosted an inaugural contemporary Craft and Design Festival. From 7-9 May, ~80 specialist makers exhibited and traded contemporary works – old and new traditional crafts and design: studio ceramics, hand-printed textiles, furniture, jewellery, glass, art, and weaving of fabrics and willow. Your annual pass gave you access to this Craft and Design Festival, and was a huge success for us!” (Indoor venue in the South East)

“May was the best month of the year so far with retail also performing better. Strong family programming help with the May numbers in school holidays.” (Roman Baths)

Venue hire may also be having a positive impact on revenue, with 30% saying performance is better than in 2025, compared to 22% describing it as worse.

Marketing also playing a significant supporting role

Finally, the latest survey highlighted some interesting marketing initiatives that are supporting commercial outcomes. English Heritage highlighted their ‘Reach’ campaign that offered national newspaper readers free entry to sites across the country, as well their national ‘£1 scone’ campaign.

“We also launched a national ‘£1 scone’ offer in conjunction with the free entry tickets to allow for footfall to convert into commercial spend. This F&B offer gained great traction on socials with humourous exchanges between peers in the sector (as well as launching the cream or jam first debate) which really saw a boost in our online socials engagement.” (English Heritage)

At The Brunel Museum, influencers have been used to drive visits.

“We’ve been running an influencer campaign to invite people with big followings to visit the museum and create content.” (Brunel Museum)

Conclusion

In summary, the sector continues to operate in challenging times, but strong commercially-friendly programming, resurgent retail and resilient venue hire is helping to counter sluggish visitor numbers. As we look ahead to the summer, let’s hope pent-up demand and a staycation surge will increase visitor numbers too.

Find out more

Members can learn much more via the Commercial Performance Barometer online dashboard where you can search by sub-group and merge months. You can also read examples of best practice in the sentiment dashboard – please do check out both links.

Listen to the latest episode of the Arts & Culture Podcast in which an expert panel discuss how commercially aligned programming can increase overall financial resilience.

For more information about the monthly Commercial Performance Barometer please contact tom@culturalenterprises.org.uk or jon.young@decisionhouse.co.uk