November 2025 results from the Cultural Enterprises Commercial Performance Barometer are now live, following responses from 141 cultural venues across the UK and Ireland, revealing a tale of contrasting fortunes amongst free and charging sites.

Key findings for this month include:

- Average admissions 2% down on November 2024

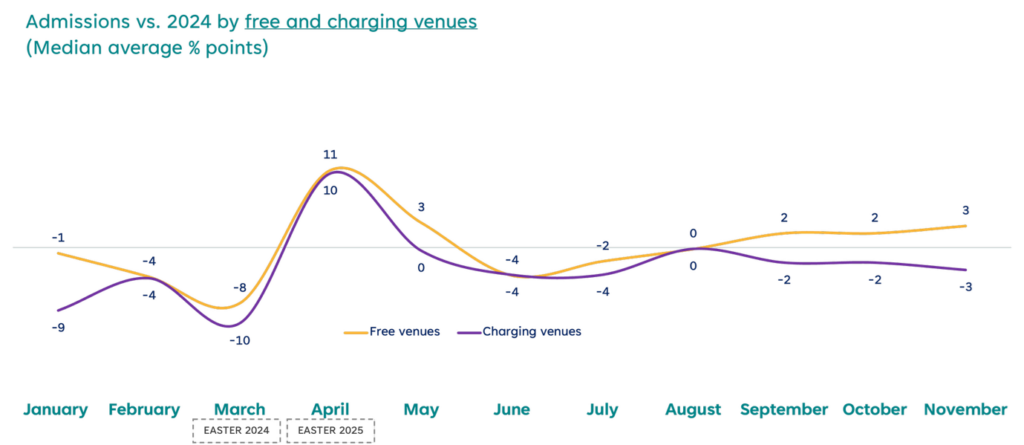

- Charging venues continuing to drive the fall at -3%

- Free venues continuing to do better at +3%

- Retail rebound confirmed.

November 2025 is the eighth month this year where the cultural sector has reported lower admissions than in 2024 at -2%. Consistent with previous months, this fall is driven by charging venues (at -3%) – free venues reporting a positive month (at +3%).

The contrasting fortunes of free and charging sites have been apparent since January, but are becoming more pronounced as we approach the year-end. November marks the third consecutive month of admissions growth for free venues, with the opposite the case for sites that charge.

The impact of admissions is also reflected in sentiment. As of November, 72% of free venues are optimistic about the next 12 months, compared to 55% of those that charge. These figures leave little doubt that the cost-of-living is having an impact on how people are selecting their leisure choices.

Retail in a stronger place as the year ends

More positively, we have now seen four consecutive months of above-inflation retail SPV growth, consistent across both free and charging venues. Whilst the increase may be indicative of a mindset shift amongst the public, individual venues are clearly impacting the change through ‘merchandisable’ programming, winter markets and new product lines:

“We launched a new exhibition with a large preview event for participants, this saw a jump in sales over one week. Without this we would have been lower than previous years. We also launched a new range that has been very popular.” (Florence Nightingale Museum)

“Our shop sales grew by 6% vs last year’s figures, again additional programming including Winter Market selling fair during which we had our strongest day this financial year helped the performance.” (Museum of the Home)

Programming is also helping to counteract declining admissions

Consistent with all of 2025, programming has helped drive performance at both free and charging venues. At Fort Nelson, admissions more than doubled and retail performed very positively as a result of their stunning ‘Standing with Giants’ exhibition:

“Standing with Giants has had a marked increase on both footfall (with the Fort fully booked until January) as well as our retail performance which is struggling to keep up with demand.”

The Discworld exhibition at Worcester City Art Gallery and Museum has had a similarly positive impact:

“Our Discworld exhibition continued to attract good visitor numbers and really supported our retail and admissions income (as Discworld is a paid exhibition).”

The BALTIC Centre for Contemporary Art highlights the wider benefits of hosting seasonal events.

“We held our annual Christmas market which increased secondary spend in the shop and café. Footfall usually drops considerably in November and December and so we try and punctuate the calendar with events we know will be popular during these months.”

So in conclusion, November findings continue to highlight the challenge for the sector, albeit indicating the potential for programming and retail to counteract cautious consumers. For free venues the picture is much more rosy, and the challenge for these venues is to capitalise on higher visitor numbers with strong secondary spend conversion.

Where to find out more

Members can learn much more via the Commercial Performance Barometer online dashboard where you can look at monthly data and view responses to each of our special questions. You can also read examples of best practice in the sentiment dashboard.

For more information about the Cultural Enterprises Commercial Performance Barometer please contact tom@culturalenterprises.org.uk or jon.young@decisionhouse.co.uk.