With the Easter holidays now behind us, insights from the Association for Cultural Enterprises’ Commercial Performance Barometer suggest it’s been a mixed start to the year so far. Jon Young, Decision House takes a look at the key findings, including tried and tested opportunities for growth during the traditionally quieter months.

Q1 Highlights

- Steady admissions in January

- A drop in admissions in February, softened by a strong half-term

- A below-par March followed by a provisionally poor Easter weekend

- Catering and retail performing well

- Weather, financial concerns and global instability the main drags on performance.

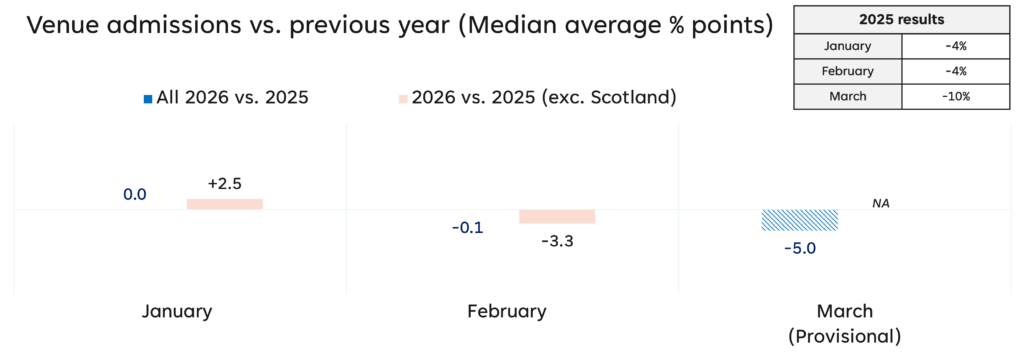

Admissions

2025 was characterised by a slow first quarter followed by seasonal peaks and a strong final quarter, and there are signs we are seeing a similar pattern emerging in 2026.

In January this year admissions were in line with January 2025, and in February they were -0.1% down. However, if we exclude Scotland (where results are dominated by membership organisations like Historic Environment Scotland and National Trust for Scotland), February figures were down -3.3% on average. Provisional figures for March suggest another month of decline, and early results suggest most venues experienced an Easter weekend that performed less well than the later Easter in April 2025.

All these figures are reported against a backdrop of decline in January to March 2025, meaning we have now seen two consecutive years of falling Q1 admissions.

Weather, Cost of Living, and Global Conflict Impacting Performance

As in 2025, weather has played a strong role in driving down visits so far this year. Venues with an outdoor offer reported a significantly bigger drop in admissions than indoor venues, and when asked to explain their commercial performance, ‘weather’ was by far the most mentioned influence. How big a factor this was depended on location of course – across the Easter weekend, for example, Scotland experienced storm and snow whilst London and the South East enjoyed days of sunshine.

Where bad weather was endured, the impact was largely felt by outdoor venues, but indirectly affected indoor venues whose commercial areas lacked capacity to meet demand.

“In February, we saw fewer visitors than last year. Weather was a massive player in this as our outdoor sites experienced closures due to winds and flooding. Our more indoor based sites don’t have the capacity in our commercial areas to support the visitor numbers wanting to stay indoors, therefore our conversion dropped alongside our KPIs.” (English Heritage).

The public’s concerns around personal finances are also a key factor. Charging venues were far more likely than free venues to report lower admissions in February, and we are seeing a slight drop in ‘non-essential’ online retail spend. With our January to February data pre-dating rising fuel prices, cost of living is likely to have more of an influence in March.

“Weather and cost of living led to a fairly flat half term.” (Imperial War Museums)

“Heavy rain, flooding and high winds greatly effected visitation and local access to some of our sites throughout January.” (Historic Environment Scotland)

In addition to impacting spending, the conflict in the Middle East may also be acting as a drag on overseas visitors. A number of March submissions mentioned this as a specific reason for a difficult month.

Reasons to be Cheerful

Positively, people who are visiting are then spending on site. In February, catering SPV (spend per visitor) was +7% on 2025, and retail was +4%, with similar results in January. This marks a shift from 2025, when retail SPV rises were consistently below inflation.

Furthermore, most venues reported a strong February half-term, with 43% saying it was better than last year and just 22% worse. Had half the country not experienced snow and storms across Easter weekend, we may have seen a similar picture then too.

Not withstanding a snowy Easter, Scottish venues may be feeling a little happier more generally. After a tricky January, they reported admissions of +2.6% in February, a trend that held strong with or without their large membership organisations.

Reasons to be Optimistic

Despite some gloomy stats to open up the year, venues remain upbeat. As of early March, 61% described themselves as very or fairly optimistic about the next 12 months (vs 58% in 2025).

Furthermore, the changeable weather appears to be impacting admissions more than financial concerns, so with increasing sunshine, we may see admissions follow suit.

It’s also reasonable to argue that financial concerns are driven by caution rather lack of funds – GfK’s Consumer Confidence Barometer reporting a big jump in their savings index. If confidence returns so may spending on days out.

Opportunities for Growth

With that all said, two consecutive years of Q1 decline suggests the sector may need to review its approach in this period. In both 2025 and 2026, admissions have been curtailed due to bad weather, so ensuring a strong indoor offer feels important.

It may also be that a lack of programming means people are lacking reasons to visit after a busy and expensive festive season. In 2025, Liverpool Cathedral’s ‘Threads through the Bible’ exhibition demonstrated what can be achieved with the right programming at this time of year.

“We have an art installation and it has been much more busy and popular than we anticipated. We have seen large increases in daily footfall and most days there have been queues out the door for the bistro and shop (and merchandise for the exhibition is selling extremely well). I think that we’ve learned that January and February don’t have to be ‘quiet’ months, as has been the case in previous years.” (Liverpool Cathedral, 2025)

As outlined by the Old Royal Naval College last year, programming in the off-peak months can also be a great opportunity to build a relationship with a local audience who need an ‘urgent’ reason to visit.

“We have found programming our installations in the winter months means we are providing an urgent reason to visit for local and UK based audiences who are also booking additional experiences and events that we are programming around the installations (something that one-off international tourists would be unable to do) and building strong relationships with those audiences.” (Old Royal Naval College, 2025)

Discover more

We look forward to exploring ways of boosting Q1 performance, along with further insights in our next Commercial Performance Barometer webinar on Friday 15 May – book your free place now.

Meanwhile, Cultural Enterprises Members can learn much more via the Commercial Performance Barometer online dashboard where you can filter by sub-group and merge months. You can also read examples of best practice in our sentiment dashboard – please do check out both links.

For more information about the monthly Commercial Performance Barometer service from the Association for Cultural Enterprises please contact tom@culturalenterprises.org.uk or jon.young@decisionhouse.co.uk.